Can IRS Garnish Spouse Wages? What You Should Know

Detail Author:

- Name : Alfonso Hagenes II

- Username : onienow

- Email : diamond58@langworth.com

- Birthdate : 1982-07-19

- Address : 371 Steuber Courts Goldaton, SD 72613-8148

- Phone : 575-501-0805

- Company : Breitenberg-Gutkowski

- Job : Religious Worker

- Bio : Id qui consequatur qui omnis ipsa nobis. Rerum aut eaque accusamus. Eum et nemo velit odit non voluptas dolorem et. Omnis minima officiis suscipit velit in accusantium minima.

Socials

facebook:

- url : https://facebook.com/nicolette_stark

- username : nicolette_stark

- bio : Ut laboriosam et iste. Consequatur numquam cumque et repellat.

- followers : 1893

- following : 1468

linkedin:

- url : https://linkedin.com/in/nicolette_stark

- username : nicolette_stark

- bio : Ut ea sequi incidunt est velit quisquam.

- followers : 2205

- following : 423

Figuring out what happens when the IRS comes knocking about a tax debt, especially when it involves your partner, can feel pretty confusing. It's a question many people ask, and honestly, it's a very important one for your household's financial well-being. Knowing if the IRS can actually take money from your paycheck for a tax bill that belongs to your husband or wife is key to protecting yourself and your family's money. This situation, you know, it can create a lot of worry, and getting clear answers helps a lot.

You might be wondering, "Will my income be on the line if my spouse owes back taxes?" That's a really common concern, and it's something many couples think about, especially if one person has a past tax issue. The answer, you see, isn't always a simple yes or no. It really depends on some specific things about how you both file your taxes and the nature of the debt itself. So, getting a good grip on these details is a pretty smart move for anyone in this spot, actually.

This article aims to clear up some of that confusion, giving you straightforward information about when the IRS might reach for your wages because of a spouse's tax debt, and when they simply cannot. We'll also look at some of the ways a spouse's tax problems can affect your shared finances, even if your own paycheck is safe. Understanding these different scenarios, it's almost like having a roadmap for what to expect and what steps you might need to consider, in a way.

Table of Contents

- Understanding Joint vs. Separate Tax Liability

- When the IRS Can Garnish Your Wages

- When the IRS Will Not Garnish Your Wages

- How IRS Wage Garnishment Works

- Protections and Limits on Garnishment

- What Property the IRS Can Seize

- Seeking Professional Help

- Frequently Asked Questions

Understanding Joint vs. Separate Tax Liability

The whole idea of whether the IRS can take your money for your spouse's tax debt really comes down to something called "tax liability." This, you know, is basically who is legally responsible for the tax bill. Married couples, actually, have a couple of choices when they do their taxes. They can file jointly, meaning they submit one tax return together, or they can file separately, where each person sends in their own return. These choices, pretty much, make a big difference for any tax debts that pop up later on.

When you file jointly, you are, in a way, agreeing to be equally responsible for everything on that tax return. This means, if there's a tax debt that comes from that joint return, both of you are on the hook for it, even if one person earned all the income or caused the problem. It's like, you know, signing a shared agreement for that money. So, that's a very important thing to consider when you choose how to file your taxes, as a matter of fact.

On the other hand, when you file separately, your tax responsibilities are, generally speaking, kept apart. If your spouse gets a tax debt from a year they filed separately, that debt, usually, belongs just to them. Your own income and assets, in that case, are not typically fair game for that specific debt. This distinction, it's almost, makes a big difference in how the IRS can act, you know, when they are trying to collect. This is a crucial point for many people, really.

When the IRS Can Garnish Your Wages

The IRS can, actually, take money directly from your paycheck if the tax debt is something you both share. This happens when you have a "joint liability," which means you are both legally responsible for that specific tax bill. So, if you and your spouse filed a tax return together and there's a debt from that return, the IRS can, and very likely will, try to get money from both of your wages to pay it off. It's like, you know, a shared financial obligation, basically.

This is a very important point for couples to grasp. If you've ever filed a joint tax return, any tax debt that comes from that particular return is, in some respects, a debt for both of you. The IRS doesn't really care whose income caused the debt or who filled out what part of the form. If your names are both on that joint return, you're both responsible. This is a situation where, you know, the IRS sees you as one unit for that specific tax year.

They can, as a matter of fact, seize tax refunds that belong to either of you, and they can also garnish wages from both of you, too. It doesn't matter who incurred the original tax liability; if it's a joint debt, both incomes are fair game. This is a scenario where, you know, your separate incomes become targets for the same judgment. So, understanding this shared responsibility is pretty key, honestly.

The Impact of Filing Jointly

When you choose to file your taxes as "married filing jointly," you are, in essence, signing up for shared responsibility for that tax year's outcome. This means, if there's a tax debt that comes from that joint return, the IRS sees both of you as equally liable for it. It's not just your spouse's problem; it's a problem for both of you. This can, you know, lead to the IRS garnishing wages from either or both of you to collect that money, as a matter of fact.

This shared responsibility extends to future actions as well. If you filed jointly in the past and there's an outstanding debt, the IRS can pursue both of you. And, you know, if you plan to file jointly again in the future, the IRS may, basically, continue to pursue both of your wages if that old joint debt is still hanging around. So, the decision to file jointly, it's almost, has long-lasting financial implications for both partners, really.

It's worth remembering that even if you've been filing separately for a while, a past joint return can still create issues. That old joint liability doesn't just disappear because you've changed your filing status. The IRS, you know, has a long memory when it comes to collecting what they believe is owed. This is why, in some respects, understanding your past filing choices is very important when looking at potential wage garnishments.

Indirect Effects on Household Income

Even if the IRS cannot directly garnish your wages because the tax debt is solely your spouse's, you might still feel the effects financially. This is a very common situation, actually. For instance, if the IRS garnishes your husband's wages for a debt that belongs only to him, that money comes right out of your household's total income. This means there's less money coming in for bills, groceries, and everything else you both rely on. So, in a way, it still affects you quite a bit.

Think about it: a wage garnishment, you know, reduces the amount of take-home pay your household receives each pay period. If your spouse's paycheck is suddenly smaller, that means less money for shared expenses, savings, or even just daily living costs. This can create a real financial strain, even if your own paycheck is completely untouched. It's like, you know, a ripple effect on your overall budget, basically.

This indirect impact can be pretty significant, especially for families that rely on both incomes to get by. A sudden drop in household funds can make it tough to meet obligations, and it might even force you to adjust your spending habits quite a bit. So, while your wages might be safe, the financial pressure on your household, you know, can still be very real. It's a situation that, in some respects, requires careful financial planning.

When the IRS Will Not Garnish Your Wages

Here's some good news for many people: the IRS generally will not garnish your wages if the tax debt is not a joint liability. This means if your spouse owes back taxes from a year when they filed as "married filing separately," or from before you were even married, that debt is typically considered theirs alone. In such cases, your individual income, you know, is usually protected from that specific garnishment. This is a pretty clear rule, actually.

Married couples, as we talked about, can choose to file their taxes either jointly or separately. If you've consistently filed separately, or if the debt originates from a period before your marriage, the IRS will typically only pursue the individual who incurred the debt. So, your wages, in that situation, are not usually subject to garnishment for your spouse's separate tax bill. This distinction, you know, is very important for your peace of mind, really.

It's important to remember, though, that even in these cases, the IRS can still seize a joint tax refund if you happen to file jointly in a subsequent year and your spouse has an outstanding debt. But for direct wage garnishment, if the liability is clearly not shared, your paycheck is generally safe. This is a key protection, you know, for individuals who have kept their tax affairs separate from their partner's past debts, as a matter of fact.

How IRS Wage Garnishment Works

When the IRS decides to garnish wages, they don't, you know, send you a personal heads-up about it directly. That's a very common misunderstanding. Instead, the IRS issues what's called a "levy notice" directly to your employer. This notice, basically, tells your employer to start taking a portion of your wages and send it straight to the IRS. So, your employer is actually the one who tells you about the garnishment, not the IRS itself, usually.

This can be a bit of a shock for people, you know, because they might not know it's happening until their paycheck is suddenly smaller. The employer, upon receiving the levy notice, is legally required to comply and begin withholding funds from your pay. This process, it's almost, bypasses you directly until your employer informs you. So, if you're worried about this, being aware of how the IRS communicates this is pretty important, honestly.

An IRS levy is a very serious matter. It permits the legal seizure of your property to satisfy a tax debt. While we're talking about wages here, it's good to know that the IRS can also take money from your bank accounts, seize and sell your vehicles, and even real estate. So, a wage garnishment is just one tool they have, you know, to collect what's owed. It's a powerful tool, as a matter of fact, that they use to get the money back.

Protections and Limits on Garnishment

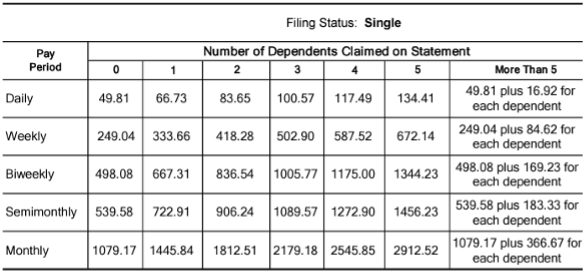

Even if the IRS can garnish your wages, there are, thankfully, some protections in place that limit how much they can take. You're not, you know, left completely without any money. These limits are designed to ensure that you still have enough income to live on, which is a pretty important consideration. So, while a creditor can put the bite on your wages, you still have some protection, basically.

One of the main protections comes from the Consumer Credit Protection Act (CCPA). This law sets limits on how much of your earnings can be garnished. It's important to know that these limits apply to various types of garnishments, including those for tax debts, child support, or alimony. The garnishment law, you know, allows for a certain percentage, but not everything, to be taken. This is a very helpful safeguard for many people, really.

For example, there are specific thresholds based on your disposable income. Disposable income, you know, is the money left after mandatory deductions like taxes and Social Security. If your weekly disposable income is $217.50 or less, the IRS can't garnish your wages at all. That's a pretty significant protection for lower earners, as a matter of fact. It ensures a basic level of income remains untouched.

Consumer Credit Protection Act (CCPA)

The Consumer Credit Protection Act (CCPA) is a very important piece of legislation that helps protect individuals from having too much of their wages taken by creditors, including the IRS. This act, you know, sets specific limits on the amount of earnings that can be garnished. It means that even if you owe a debt, the creditor can't just take your entire paycheck. There are rules, basically, about how much they can legally collect from your wages.

These wage garnishment provisions, you know, are particularly relevant for court orders related to child support or alimony, but they also apply to tax debts. The law aims to strike a balance: allowing creditors to collect what's owed, but also ensuring that individuals have enough money left to cover their basic living expenses. So, it's a kind of safety net, you know, for your financial survival, really.

The specific amount that can be garnished under the CCPA often depends on factors like your income level and whether you are supporting other dependents. This means the percentage of your wage subject to garnishment, you know, is not a fixed number for everyone. It's something that changes based on your personal situation. So, understanding these limits is pretty vital if you're facing a garnishment, honestly.

Income Thresholds and Dependents

The IRS has specific rules about how much of your wages they can take, and these rules are tied to your disposable income. For instance, if your weekly disposable income is between $217.50 and $290, the IRS can only garnish anything above that $217.50 mark. So, if you make $250 in disposable income a week, they can only take $32.50. This is a very clear limit, you know, that helps protect a portion of your earnings, basically.

Furthermore, if you are supporting another spouse or a child, the garnishment limits can be different. For someone supporting a spouse or child, up to 50% of their disposable earnings can be garnished. This is a pretty significant amount, but it's still a limit. However, if the individual is not supporting another spouse or child, that limit, you know, can be higher, sometimes reaching up to 60% or even 65% in some cases. So, your family situation actually plays a big part.

These thresholds and percentages are put in place to ensure that people still have enough money to meet their basic needs, even when facing a tax debt. While common law states, you know, might offer more protection in some scenarios, there are still situations where spouses' wages are vulnerable to garnishment, especially with joint debts. So, knowing these specific numbers and rules is pretty crucial, honestly, when you're looking at your own situation.

What Property the IRS Can Seize

An IRS levy is a very powerful tool that allows the government to legally seize your property to satisfy a tax debt. It's not just about your wages, you know; they have a much broader reach. While wage garnishment is a common method, the IRS can also take money directly from your bank or other financial accounts. So, any funds you have saved up could be at risk, basically, if you have an outstanding tax debt.

Beyond cash and wages, the IRS can also seize and sell other valuable assets you own. This includes things like your vehicle or vehicles, which can be a real blow for many families. They can also go after real estate, like your house or other properties you might own. So, an IRS levy, you know, permits the legal seizure of a wide range of your property to satisfy a tax debt, as a matter of fact.

It's important to grasp the full scope of what the IRS can do when they issue a levy. It's not just a minor inconvenience; it's a serious action that can significantly impact your financial life and your assets. Whether you're the one who incurred the tax liability or your partner, the IRS can seize tax refunds, garnish wages, and take other property if the debt is a joint one. This is why, you know, acting quickly when you receive notices is very important.

Seeking Professional Help

If you've received notices in the mail that the IRS wants to garnish your wages due to a tax debt, especially one related to your spouse, it's a very good idea to get professional help. An attorney who specializes in tax law, you know, can be incredibly helpful in this situation. They can assist you in understanding your rights and figuring out the best steps to take to try and stop the garnishment. So, reaching out for expert advice is pretty smart, honestly.

Whether a spouse's wages can be garnished for a debt not in their name depends on a lot of specific details, as we've discussed. A qualified tax attorney can look at your particular situation, review your filing history, and determine the exact nature of the tax liability. This kind of expert review, you know, is very important for understanding your options and what might be possible. It's almost like having a guide through a complicated process, basically.

They can also help you explore potential solutions, such as setting up an installment agreement with the IRS, applying for "innocent spouse relief" if that applies to your situation, or even negotiating an "offer in compromise." These are complex processes, and having someone who knows the ins and outs of tax law can make a huge difference in the outcome. So, if you are suffering a wage garnishment, or fear one is coming, contacting a professional is a very wise move, really.

Frequently Asked Questions

Here are some common questions people ask about IRS wage garnishment and spouses:

Will the IRS garnish my wages if my spouse owes back taxes?

No, the IRS will not garnish your wages if the tax debt is not a joint liability. If your spouse's back taxes are from a year they filed separately, or from before your marriage, your individual wages are generally protected. However, if you filed jointly for the year the debt was incurred, then yes, the IRS can and likely will garnish both of your wages in that situation. It really depends on how you filed your taxes for that specific year, you know, when the debt came about. So, understanding that joint versus separate filing is very key, basically.

Does my spouse's tax liability affect me?

Yes, your spouse's tax liability can affect you, even if your wages aren't directly garnished. If the IRS garnishes your spouse's wages, it reduces your total household income, which means less money for shared expenses and bills. Also, if you file jointly in the future, the IRS may, you know, seize a joint tax refund to satisfy your spouse's separate debt. So, while it might not always be a direct hit to your paycheck, there are definitely financial ripple effects that can impact your shared finances, as a matter of fact.

What can an attorney do to help with an IRS wage garnishment?

An attorney can help you understand your rights and take steps to stop or reduce the garnishment. They can review your tax situation to determine if the debt is truly a joint liability or if you qualify for relief, like "innocent spouse relief." They can also help you communicate with the IRS, negotiate payment plans such as an installment agreement, or even propose an "offer in compromise" to settle the debt for a lower amount. So, having a legal expert on your side, you know, can make a big difference in how you deal with the IRS and protect your finances, really.

Understanding the factors that determine your liability is the first step when facing potential IRS action. Whether you're the one who incurred the tax liability or your partner, the IRS can seize tax refunds and garnish wages under certain conditions. So, knowing your situation is pretty important, honestly. You can learn more about tax relief options on our site, and if you need specific guidance, you might want to consider contacting a tax professional for personalized advice. It's almost like having a plan, you know, for what to do next.

{kind=link}